Week 4: Deep Dive into Demographics

March 21, 2026

Hello everybody, I hope you guys are all having a great week. Welcome back to week 4 of my senior project blog! This week, unfortunately, I wasn’t able to get through everything I tried to do this week, but I still got through about 90% of what I wanted to, which is great!

Demographic Duties

This week, my goal was to both create and finalize my five personas that I will use for evaluation, and complete the second agent in the sequential pipeline. I decided to first start with creating the five personas, and I did some demographic research into personal financial knowledge in the United States. I decided to only focus on the United States as expanding this to foreign countries would require me to supplement knowledge to the LLM far beyond what I currently have, and it would cause me to get significantly closer to the token memory limit of the LLM, which is not something I wish to do.

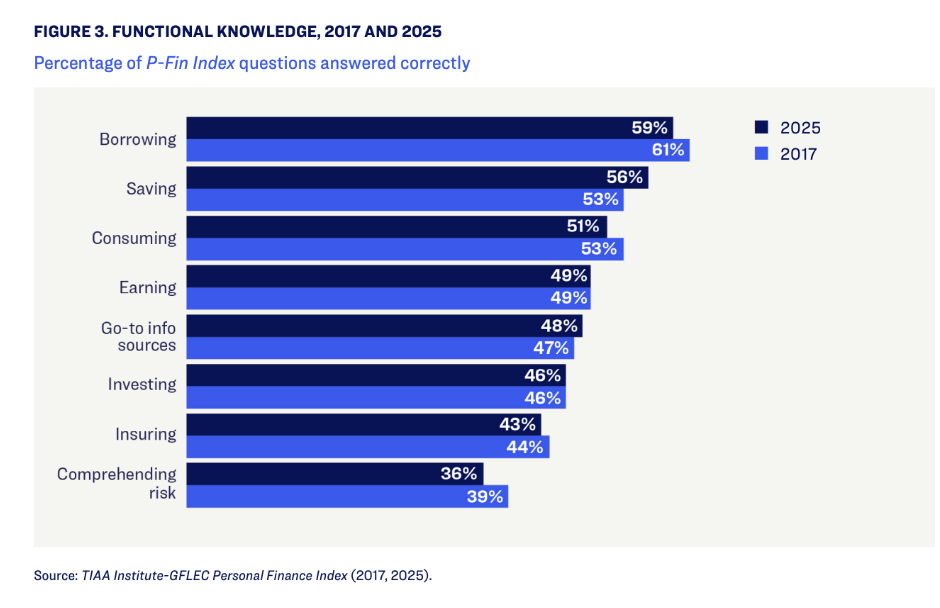

The TIAA Institute publishes an index known as the GFLEC Personal Finance (P-Fin) Index annually [1] . The P-Fin index is a financial readiness exam which assesses the US adult population on their ability to make sound financial decisions across eight common financial activities: earning, consuming, saving, investing, borrowing, insuring, understanding risk, and gathering information.

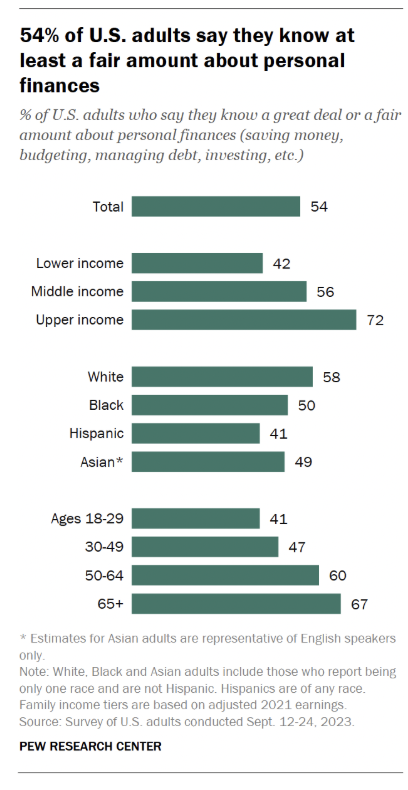

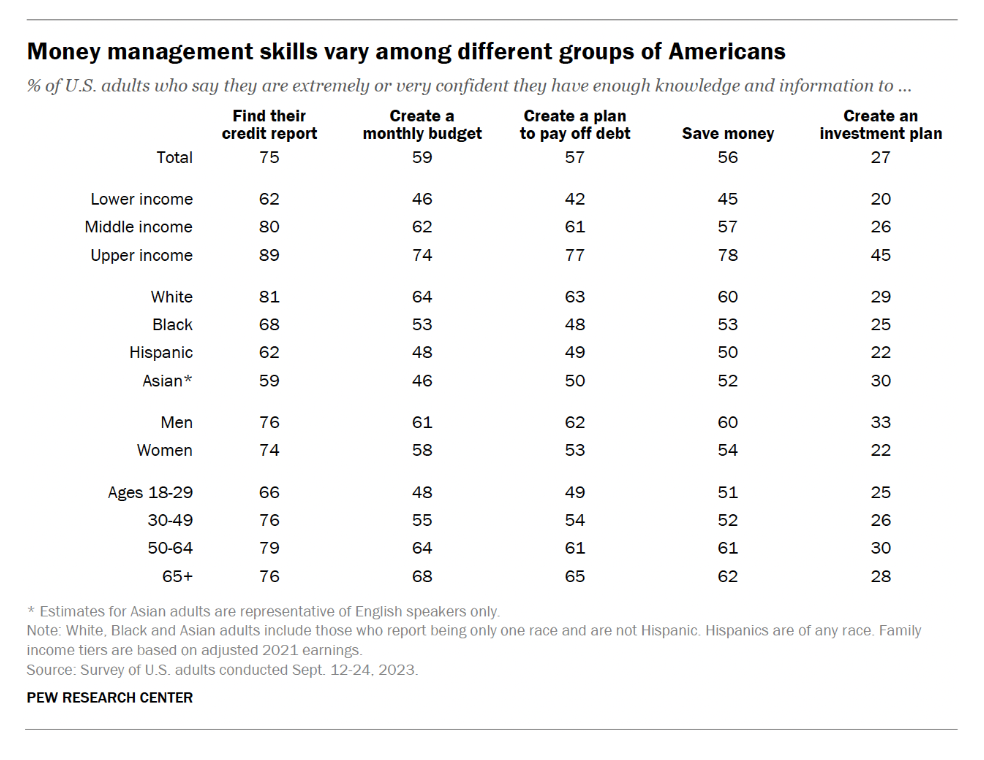

Likewise, I also took a look at the Pew Research Center’s demographic data [2] , which measured people’s personal opinion on how much they THOUGHT they knew about personal finance. This is just as important to knowing how well people actually know about personal finance because it gives us a concept as to the disparity between people’s perception of themselves versus what reality actually says (the P-Fin Index).

The Personas

Now it’s finally time for me to show you the personas, and here they are!

Persona 1: recent college grad entry-level salary hispanic individual living in an HCOL area (most likely west coast) with significant student debt. Key stress test: Can the system create a well structured plan to pay off student loans and begin creating an investment plan?

Persona 2: middle-aged white career professional with stable mid-income living in suburban city with a family, no significant debt, wants to retire early and begin investing. Key stress test: Can the system sense that this individual is in a well-off financial situation and expand expectations to take risks and make money moves that are limited by heuristics?

Persona 3: young black skilled freelance worker in a medium COL city with inconsistent monthly income (bouncing from low to mid) and no employer 401(k), wants to stabilize and settle down. Key stress test: Can the system deal with variable income and plan for future savings without employer matching?

Persona 4: middle-aged white single parent with two young children, moderate income in a suburban area, wants to save for college in the next 10 years. Key stress test: Can the system deal with needing to save a large sum of money in a relatively short timeframe without largely cutting down on the quality of life?

Persona 5: Near-retiree with high net worth, poor asset allocation, and significant credit card debt, working a stable job in a city. Key Stress Test: How does the system deal with high credit card debt this close to retirement? (missing age and income level)

Each key stress test is a way to test the architecture and stretch it in a way that would be difficult even for a human financial advisor to accomplish. As a result, I plan to use these as the baseline tests across the control group and the 3 experimental groups. If time permits, I plan to create more, but for now I am going to stick to 5 personas.

Agent 2 (Incomplete, Unfortunately)

The next part of my week was to work on Agent 2 in the sequential pipeline, the heuristic strategist, but however due to the time this background research took and my duties in Science Olympiad, I was unable to complete more than just a draft of the system prompt, which I hope to refine. In time for next week, I will create a python script (which I already have the skeleton for), and update my GitHub along with my future work on Agent 3 next week.

Eventually, I also plan to move all my agents from running locally on my device through the Gemini API and move them to Google ADK, a python framework for running agents. I’ll talk more about those next week, so stay tuned and thanks for reading!

Sources

[1] Financial Literacy and Retirement Fluency in America, www.tiaa.org/content/dam/tiaa/institute/pdf/insights-report/2025-05/financial-literacy-and-retirement-fluency-in-america-p-fin-ir.pdf. Accessed 21 Mar. 2026.

[2] Edwards, Khadijah. “Personal Finance Knowledge and Confidence Vary by Income, Race, Age in the US.” Pew Research Center, Pew Research Center, 9 Dec. 2024, www.pewresearch.org/short-reads/2024/12/09/roughly-half-of-americans-are-knowledgeable-about-personal-finances/.

Reader Interactions

Comments

Leave a Reply

You must be logged in to post a comment.

This was a really interesting update! I liked how you used actual data (like the P-Fin Index) to shape your personas, making them a lot more realistic than just random, AI-generated personas. I was wondering how comprehensive you think these personas will be across all real-world cases, and if you anticipate any unique obstacles for each persona you might face in getting the agents to provide authentic, applicable advice?

Hello Aanya,

Thanks for your comment! I based the personas off of demographic groups that had the least personal confidence in their own financial ability (according to the Pew Research Report), and also in topics specifically that people struggled with in general. I believe that for Personas like 4 and 5 may run into some issues particularly with Agent 3 in the sequential pipeline as they are purposefully vague descriptions meant to stress test that part of the system.

I really found this to be a cool blog post and I especially like how you were able to find and effectively use real-world financial data. More specifically, I especially like how you decided to limit the scope of the personas so that the framework is tested for a specific achievable thing, rather than aiming for an overly broad goal that’s unattainable. However, with respect to the personas, I agree with Aanya and I was wondering do you think that these 5 personas alone will be enough to test cases restricted to the US? In other words, how confident do you feel that these 5 personas can properly test the framework to the extent it could be used in real life and prevent holes in knowledge or weird results in any edge cases?

Hello Ethan,

Thanks for your comment! Five personas is mostly just a base number of cases I chose to work with when planning this project, as I wanted to focus more of my time on designing and building the system architecture. Due to the constraints of the senior project and the limited timeframe I’m conducting this over, my goal is to add more test cases (up to 10) in order to get a broader overall testing set. Also, I plan to make a survey and test the final product amongst various adults to attempt to get a more realistic standard of its viability. There is no way to cover every angle or financial situation but for the scope of this project, this should be enough data to come to relatively sound conclusions.